What can the first blockchain antitrust case teach us about the crypto-economy?

Konstantinos Stylianou

Konstantinos is an Assistant Professor in Competition Law and Regulation and the Deputy Director of the Centre for Business Law and Practice at the University of Leeds School of Law. He holds an S.J.D from the University of Pennsylvania, an LL.M. from Harvard University, and a Bachelor's and Master's in Law from Aristotle University. During the Spring Semester 2019 he is a Visiting Scientist at Brown University Department of Computer Science.

Of all the areas blockchain has made headlines in, antitrust has ranked fairly low. To the extent that there have been disputes or regulatory activity, they have so far revolved around the financial aspects of cryptoassets and less so around market distortions, which is antitrust’s domain. But where there is money there is power, and where there is power there is abuse of power, and so it was only a matter of time until an antitrust claim would arise. In December 2018, UnitedCorp, a diversified technology company, sued Bitmain, the largest Bitcoin mining pool, and a number of other high-profile stakeholders in what was the first blockchain dispute with a focus on antitrust (United American Corp. v. Bitmain, Inc. Complaint).

The case is complex, not least because of the technical details and the convoluted alleged anticompetitive scheme. But at its core one finds a familiar collusion claim. Interestingly, the filing attorneys are corporate/financial law experts—not antitrust experts—perhaps indicative of the fact that cases involving blockchain, and in particular Bitcoin, continue to be lumped together under financial regulation.

The case is currently pending before the District Court for the Southern District of Florida. It is hard to predict how much the court will engage with the case. In all its boldness, the complaint leaves a lot to be desired, as it fails to map the facts and legal claims onto the requirements of the allegedly violated Section 1 of the Sherman Act. That said, the case opens for the first time a window into how the crypto-economy can malfunction in a way that harms consumers and the competitive dynamics of the industry.

Facts and Background

UnitedCorp offers a number of blockchain solutions, including BlockNum, which allows the execution of blockchain transactions using regular phone numbers, and BlockchainDome, which is a cryptocurrency mining system that uses the heat generated from the mining process to heat greenhouses for agricultural purposes. Both technologies rely on a cryptocurrency called Bitcoin Cash.

Bitcoin Cash was one of the hundreds of publicly available (permissionless) cryptocurrencies and, much like any other cryptocurrency, its rules and governance were specified in its whitepaper and protocols and were followed by the miners who mined and validated the transactions on the Bitcoin Cash network. In November 2018, Bitcoin Cash was scheduled for a routine upgrade of its protocols. However, the protocol developers disagreed on the new rules, which resulted in a split between two different camps, called forks: Bitcoin ABC and Bitcoin SV. When splits like this occur, it is up to miners to choose which fork they prefer to support (by mining for their preferred fork). In this case a protracted battle between the two forks to gain miners’ buy-in broke out causing the combined value of the two forks to drop below the levels of the formerly unified Bitcoin Cash cryptocurrency before the forking. Of the two forks, Bitcoin ABC garnered greater support and succeeded Bitcoin Cash in name and in ticker (BCH).

Allegations

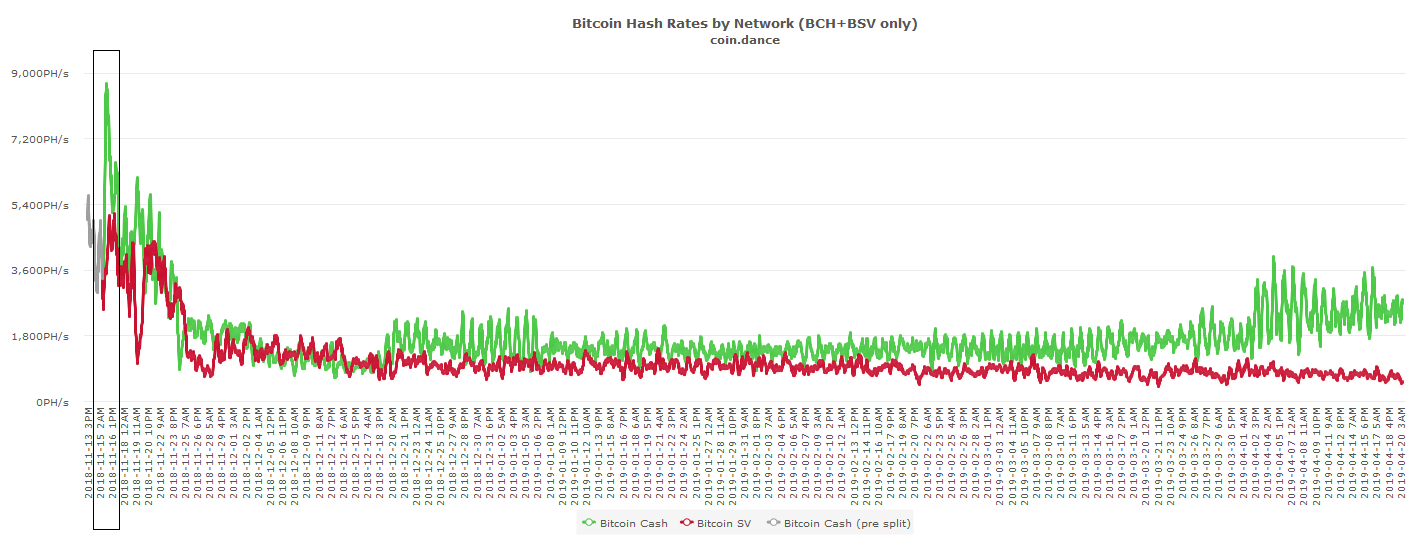

UnitedCorp alleges that a number of investors, mining pools (groups of miners that combine their mining resources), crypto-exchanges, and protocol developers colluded to get as many miners as possible to support the Bitcoin ABC fork over the Bitcoin SV fork (Figure 1). In particular, UnitedCorp claims that the colluding actors “manipulated the cryptocurrency market for Bitcoin Cash” by “centralizing what is intended to be a decentralized transactional system enabling the corruption of the democratic and neutral principles of the Bitcoin Cash network.” As a consequence of the collusion, the prices of both forks fell to levels below those of the unified Bitcoin Cash cryptocurrency before the forking, resulting in financial harm. UnitedCorp claimed that “the economics of [its offerings] depend on mining Bitcoin Cash within normal market conditions,” and therefore, the collusion, by upsetting normal market conditions, accounted for the subpar performance of UnitedCorp’s investments.

Figure 1: Hashrate, which is a proxy for mining capacity, for Bitcoin ABC (green) and Bitcoin SV (red). Notice the green spikes on and after the fork on November (boxed) 15 indicating sudden influx of hashing power from miners. Source: Coin.dance

Does UnitedCorp have standing?

As this is the first blockchain antitrust case to make it to court, it is interesting to ask even the basic question of who in the crypto-economy can actually bring an antitrust case. In antitrust cases between private parties, the plaintiff has standing if they can prove that the actions of the defendant harmed them (“any person who shall be injured in his business or property by reason of anything forbidden in the antitrust laws may sue therefor [sic]” (Section 4 of the Clayton Act). In fact, the courts have interpreted this requirement to mean that the injured plaintiff must prove that they were directly harmed by the defendant’s actions, not just that they incurred a measure of harm doing business somewhere along the value chain (Illinois Brick Co. v. Illinois). This is a particularly timely point as this requirement is at the core of litigation against Apple currently pending before the Supreme Court (Apple v. Pepper). While the facts in Apple v. Pepper differ, as the case revolves around whether app users are directly harmed by Apple’s allegedly monopolistic surcharge on the apps distributed through its App Store, the case is the first one to revisit the question of private standing in the digital economy, and therefore useful insights on the renewed interpretation of the doctrine are expected. The answer to the question for UnitedCorp in particular requires a look into UnitedCorp’s role in the value chain and into whether UnitedCorp was from that role the first in line to incur the harm caused—if any.

Where does UnitedCorp fit in the crypto-economy value chain?

UnitedCorp does not specify in what capacity it was harmed. This, in turn, makes it difficult to assess the extent of the harm it may have incurred and whether it was the first in line to incur it. There are a number of possibilities:

- UnitedCorp as investor: If UnitedCorp claims financial losses as an investor in Bitcoin Cash or as an entrepreneur in the broader cryptocurrency market, it does not seem to have a claim against anyone. None of the stakeholder-defendants provides direct investment services to UnitedCorp. In this case, UnitedCorp seems to have simply made a bad bet when it decided to sell products and services that relied on Bitcoin Cash, and antitrust law is irrelevant.

- UnitedCorp as miner: If UnitedCorp claims damages as a miner (it owns mining equipment), then the court would have to determine who provides services directly to miners. The most plausible answer seems to be protocol developers, for they provide the infrastructure on which miners operate. This answer, however, leads to a different problem, which is that it is not at all certain that the “service” provided by protocol developers is the kind of service antitrust law is concerned with. Antitrust law safeguards commercial activity by undertakings. It is immaterial whether the activity in question is provided for free or not (participation in Bitcoin Cash is free), insofar as it is economic in nature, i.e. it is meant to be part of commerce and the market mechanism. It is not obvious that the development of blockchain protocols fulfills this requirement, as it can be characterized as a research, educational, or generally non-market project. The fact that blockchain protocols can be used to underpin market-related activities does not make the development of blockchain protocols inherently commercial the same way that contributing to the development of Linux does not necessarily make a programmer a market actor, even though versions of Linux are sold commercially. Crypto-exchanges and wallets also seem to provide services to miners by channeling transactions toward them. However, without a more specific factual setting, the direct service recipients of crypto-exchange and wallets seem to be users/spenders, who in turn generate transactions that miners will process, and therefore the relationship between UnitedCorp as miner and the named crypto-exchange/wallet defendant would not satisfy the direct harm requirement.

- UnitedCorp as spender: If UnitedCorp claims to be acting as a spender of Bitcoin Cash, presumably as operator of its BlockNum system, then the most likely direct service provider would be miners, for it is miners that process the transactions proposed by users/spenders. But the facts in the complaint do not explicate how BlockNum operates and whether its operation would support a theory of UnitedCorp as spender.

Was there any antitrust-related harm?

UnitedCorp does not quite link the financial losses it claims it incurred to what antitrust law would normally accept as harm. For antitrust law purposes, harm is by and large construed as consumer harm, or, under a more liberal interpretation, harm to the competitive process. Can collusion to influence (manipulate?) a cryptocurrency’s governance system result in harm of the kind that antitrust law would acknowledge?

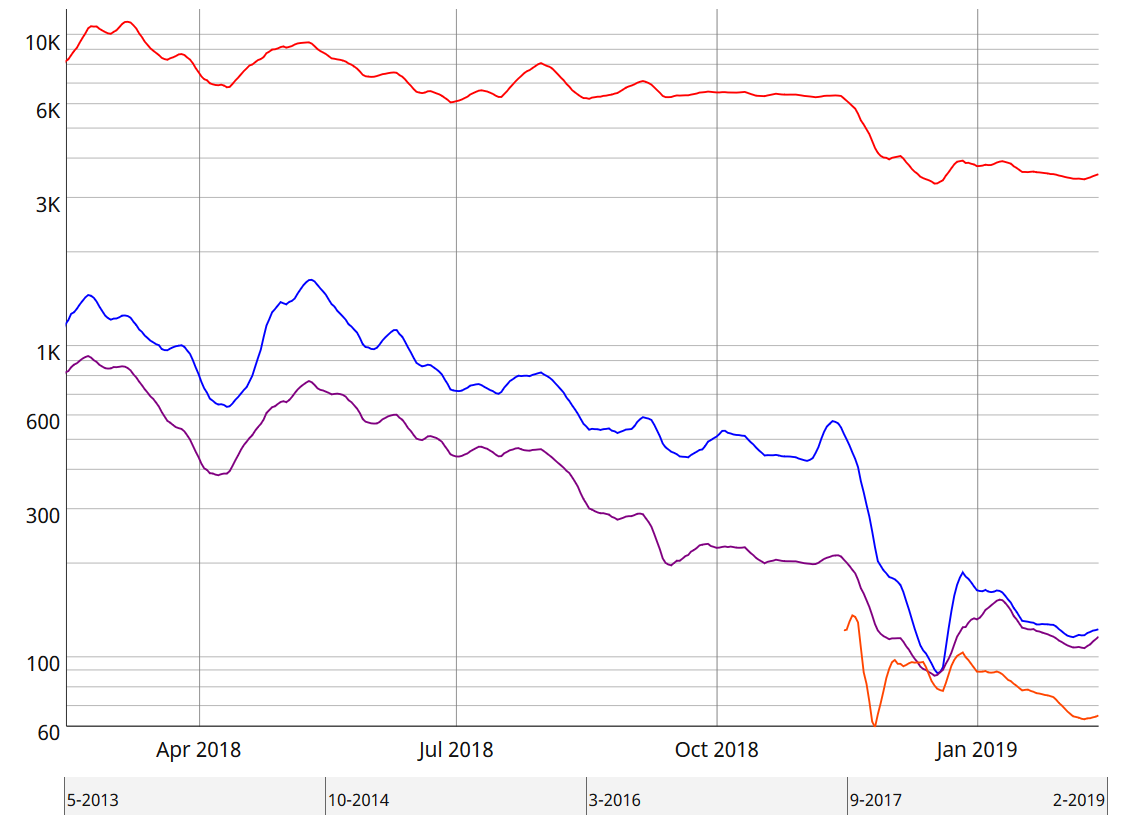

In terms of consumer harm, the only relevant allegations seem to be around how Bitcoin Cash’s devaluation might translate into harm for UnitedCorp of the kind that antitrust law would recognize. This partly links back to UnitedCorp’s role in the ecosystem: did BitCoin Cash’s devaluation hurt UnitedCorp as investor because it dampened interest into and sales of its offerings? Did it lower its profits as miner because the forking controversy limited the number of transactions or lowered the fees payable to miners? Or did it hurt it as spender because the devaluation of the currency somehow raised its costs in its BlockNum system? Importantly, what is the timeframe for the assessment of harm and how does UnitedCorp isolate the factor of the fork controversy from all other contributing factors that are unrelated to the dispute and may have well affected Bitcoin Cash’s price? As Figure 2 shows, Bitcoin Cash’s price dip in November was not only temporary, but also in line with the price movements of other major cryptocurrencies like Bitcoin and Ethereum, which might suggest that other market-wide factors were at play.

Figure 2: Price in USD of Bitcoin Cash (blue) compared to Bitcoin (red), Ethereum (purple) and Bitcoin SV (orange). Source: Coinmetrics

If one is willing to take a broader approach and include guarding against harm to the competitive process as a relevant goal of antitrust law, then this would require that UnitedCorp somehow is in competition with the defendants, and that their actions harmed it through distorting the competitive process. This claim seems even less likely to succeed. Even assuming that UnitedCorp is competing in any of the relevant markets, in none of them does it establish harm to the competitive process; it only establishes harm to a competitor, itself. For antitrust purposes, harm to an individual competitor without evidence of harm to competition is not enough to establish an offense. Whether the relevant markets are defined as mining for Bitcoin Cash, mining for cryptocurrencies similar to Bitcoin Cash, or provision of mining or blockchain transaction systems (BlockNum and Blockchain Dome), UnitedCorp hardly demonstrates reduction of competitive intensity, and therefore it is likely that this claim would fail.

If there was collusion, was it anticompetitive?

UnitedCorp alleges that defendants, including investors, mining pools, crypto-exchanges, and protocol developers, conspired with each other to transfer hashing power to the mining of Bitcoin ABC and to steer market participants away from Bitcoin SV. They did so, according to UnitedCorp, by shifting mining capacity from other cryptocurrencies to Bitcoin ABC and by presenting Bitcoin SV as unreliable. This not only harmed Bitcoin SV specifically, but it undermined trust in Bitcoin Cash generally, which allegedly contributed to the price drop.

Assuming that some kind of collusion to the effect claimed by UnitedCorp took place (and this is not self-evident both because it would be very expensive, but also because stakeholder interests may have just been aligned anyway with no need for collusion), was it an unreasonable restraint of trade that would have made it anticompetitive? Perhaps, but by a long stretch.

For one thing, defendants’ campaign to bring in hashing power into the Bitcoin Cash network seems like capacity expansion to capture a bigger share of the market (mining for Bitcoin ABC), which is hardly anticompetitive absent any other aggravating circumstances. Antitrust law is usually concerned with output limitations that result in price hikes, not output increases that end up serving more of the demand.

Secondly, it wasn’t just Bitcoin ABC that ramped up hashing power—both sides did. This, in fact, is normal and expected in forking: competing forks want to garner the support of the majority of miners and miners are more likely to build on the longer chain, which creates a snowball effect, whereby the longer a forking chain becomes the more likely it is that miners will build on it making it yet longer. Therefore, the mobilization of mining capacity may be seen as the means by which fork camps compete, which is the opposite of what an anticompetitive agreement aims at or achieves in effect.

Thirdly, even if the crux of UnitedCorp’s complaint was not the fact that miners coalesced to influence the winning camp but rather the fact that the process was manipulated to the effect that the mining results did not come about organically or naturally, it is uncertain this argument would stand. UnitedCorp bases this claim on two grounds: first, an interpretation of Bitcoin’s whitepaper, according to which the mining process is supposed to be “decentralized” and “democratic;” and second, on the fact that Bitcoin Cash developers added a checkpoint into the code shortly after the split to prevent modifications. Checkpoints are code that prevents the protocol from reorganizing blocks below the checkpoint block, thereby ensuring that even if someone acquired control of the majority of mining power, they could not change the blockchain before the checkpoint. UnitedCorp saw that as a means for Bitcoin Cash ABC developers to solidify the status of the blockchain as it resulted from the manipulated mining process. These arguments may not carry sufficient weight to conclude that the restraint of trade was unreasonable. First, whitepapers are not binding nor do they mandate an industry modus operandi from which actors are not supposed to deviate. There is nothing that says cryptocurrencies should be inherently decentralized or democratic, nor that this is the most efficient or welfare-maximizing organization of the market, such that tampering with these principles would run afoul of antitrust laws. Second, checkpoints, while controversial from a governance point of view, are not uncommon, and they are generally seen as a security and efficiency mechanism (Figure 3). These uses provide for legitimate justifications that antitrust law recognizes as potential defenses to competition law offenses. For the court to find that checkpoints were nevertheless anticompetitive, it would either have to establish that these uses were inapplicable in this particular case, or that their anticompetitive effects manifestly exceeded their procompetitive benefits.

Figure 3: Screenshots showing Satoshi’s comment on addition of checkpoints in the Bitcoin chain (top), and Bitcoin SV’s chain with checkpoints (bottom). These can be seen as evidence that checkpoints are not an uncommon practice.

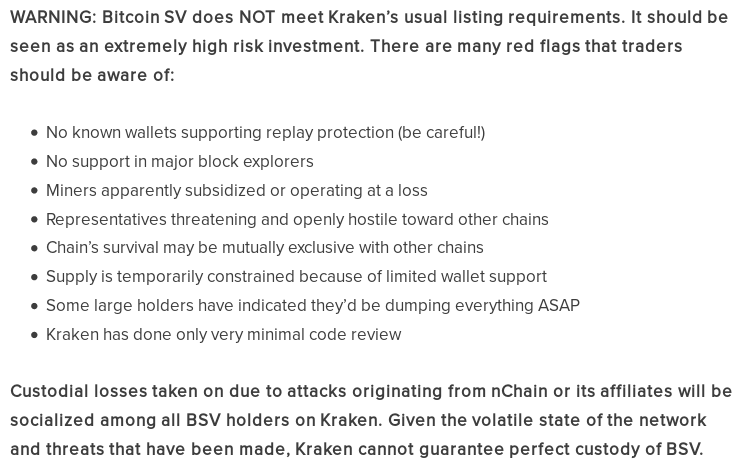

Further, UnitedCorp’s decision to include Kraken, a popular exchange/wallet, among the defendants may imply a potentially colorable collusion claim between mining pools and exchanges/wallets. Exchanges/wallets can influence spender behavior by steering them toward transactions in one cryptocurrency over another. Here, UnitedCorp claims that Kraken presented Bitcoin SV as unsafe (Figure 4), thereby channeling users toward alternatives like Bitcoin ABC. Collusion between exchanges/wallets and mining pools, which mine the transactions that exchanges/wallets facilitate, could have the effect of limiting the competitive dynamics among cryptocurrencies and of robbing users of free (unmanipulated) choice of their preferred cryptocurrency.

Figure 4: Screenshot from the popular exchange Kraken showing the cautionary note on Bitcoin SV trading.

Implications and outlook

United American Corp. v. Bitmain provides an ideal setting to assess the role of crypto-economy players and the limits of the legality of their business conduct. The case’s focus on federal antitrust law is unprecedented, and it will be interesting to see how the court approaches the questions raised therein, especially in comparison to a similar case filed in California against Coinbase, a popular crypto-exchange, whose legal basis is California’s state unfair competition law (which is broader in scope than the Sherman Act). But, legal arguments aside, this case is also rich in conspiracy theories and investor drama, which provides a rare behind-the-scenes glimpse into the interests that make the crypto-economy spin.

It is questionable whether the lawsuit will achieve its goal. Doing so would establish legal firsts whose consequences can extend far beyond the boundaries of the case itself. To uphold, for example, that mining mobilization can underpin an antitrust offense would risk serving as an implicit acknowledgement of the legal bindingness of cryptocurrency whitepapers and their decentralization and democratic ideals. This, in turn, can add pressure onto other areas of law and policy-making. For example, whitepaper stipulations have been a source of confusion and friction in financial regulation, where authorities have departed from the descriptions and characterizations found in whitepapers when classifying cryptoassets under existing regulated categories (e.g. while most cryptoasset whitepapers emphasize decentralization, the SEC has considered classifying some of them as securities, whose definition requires some sort of centralized management and decision-making). Similarly, an acknowledgement of standing for UnitedCorp under any of the above-mentioned capacities would serve as an illustration of how the legal system views the structure of the cryptoasset value chain, since it would establish a direct commercial relationship between two players of the crypto-economy. In turn, a conclusion on who provides services to whom in the market can be influential for taxation purposes and broader economic policy.

On the other hand, if the court is inclined to reject the plaintiff’s claims, it should carefully delineate the contours of the procedural and substantive standards and requirements that are expected to be met for a successful case. A broad-sweeping exclusion of cryptoasset activities or actors from antitrust’s ambit can spell unanticipated challenges in future cases, when both the nature of the activities and the role of the actors will be clearer. The temptation for broad rejections is especially strong in UnitedCorp’s case due to the all-encompassing nature of its allegations, as opposed to other legal cases where the questions at hand were much narrower in scope, which accordingly limited the scope of the court’s decision as well. For instance, the Court of Justice of the European Union (CJEU) is recently said to have declared that Bitcoin is currency, yet the CJEU only answered the very limited question of whether the service of Bitcoin exchange for fiat money falls under the “currency exemption” of Council Directive 2006/112/EC on the common system of value added tax. Such narrow decisions are less likely to predispose the outcome of future cases when a clearer and more accurate understanding of the industry in question will be available.